Featured

Table of Contents

Plans can additionally last till defined ages, which in many instances are 65. Beyond this surface-level details, having a better understanding of what these plans entail will aid guarantee you buy a plan that meets your requirements.

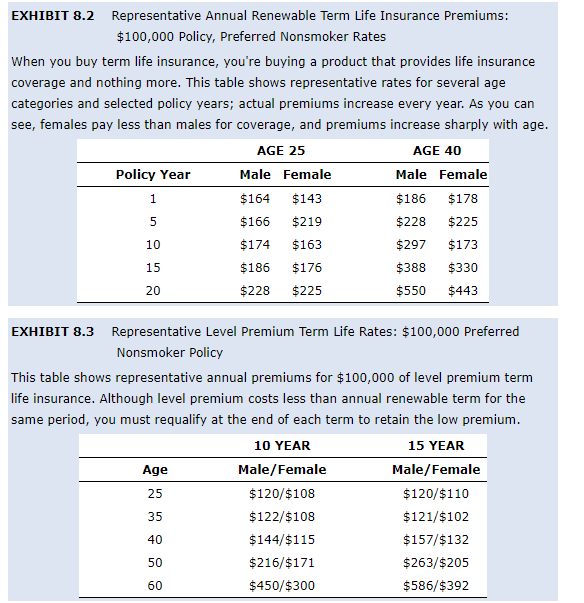

Be mindful that the term you pick will certainly affect the costs you pay for the policy. A 10-year level term life insurance policy plan will cost much less than a 30-year policy because there's less chance of an occurrence while the plan is energetic. Reduced danger for the insurance provider equates to decrease costs for the insurance holder.

Your family's age must likewise influence your plan term selection. If you have young kids, a longer term makes sense due to the fact that it safeguards them for a longer time. However, if your children are near their adult years and will be economically independent in the future, a shorter term may be a much better fit for you than an extensive one.

Nonetheless, when comparing entire life insurance policy vs. term life insurance coverage, it's worth noting that the last commonly sets you back less than the previous. The outcome is more protection with lower costs, supplying the ideal of both worlds if you require a substantial amount of insurance coverage however can't afford a much more costly plan.

How Does What Is A Level Term Life Insurance Policy Benefit Families?

A degree death benefit for a term plan generally pays as a lump amount. When that occurs, your beneficiaries will obtain the whole amount in a single payment, which quantity is ruled out earnings by the internal revenue service. Those life insurance earnings aren't taxable. Nonetheless, some level term life insurance policy firms permit fixed-period repayments.

Passion payments received from life insurance policy policies are considered income and are subject to tax. When your level term life policy ends, a few different points can occur.

The drawback is that your sustainable level term life insurance will certainly come with greater costs after its first expiration. Ads by Cash.

Life insurance policy business have a formula for determining danger making use of mortality and rate of interest (Level premium term life insurance policies). Insurance companies have countless clients taking out term life plans at once and utilize the premiums from its active plans to pay enduring recipients of various other plans. These business make use of mortality to approximate exactly how many people within a particular team will file fatality claims annually, which details is utilized to determine ordinary life expectancies for possible insurance holders

In addition, insurance provider can invest the money they receive from costs and raise their earnings. Given that a degree term plan doesn't have cash worth, as an insurance policy holder, you can't spend these funds and they do not supply retired life income for you as they can with whole life insurance policy policies. The insurance coverage firm can spend the money and earn returns.

The list below section information the advantages and disadvantages of degree term life insurance. Foreseeable premiums and life insurance policy coverage Streamlined plan structure Possible for conversion to permanent life insurance policy Minimal coverage period No cash worth build-up Life insurance costs can increase after the term You'll discover clear benefits when contrasting level term life insurance to various other insurance types.

Why You Need to Understand What Is A Level Term Life Insurance Policy

From the minute you take out a plan, your premiums will never ever change, helping you plan financially. Your protection will not vary either, making these policies effective for estate planning.

If you go this route, your premiums will certainly increase but it's constantly good to have some adaptability if you want to maintain an active life insurance policy policy. Sustainable level term life insurance is another choice worth thinking about. These plans permit you to maintain your present plan after expiration, supplying flexibility in the future.

What Makes Level Premium Term Life Insurance Unique?

You'll pick a coverage term with the best level term life insurance prices, however you'll no longer have protection once the strategy expires. This drawback can leave you clambering to find a new life insurance coverage policy in your later years, or paying a premium to prolong your present one.

Several whole, global and variable life insurance policy plans have a cash worth element. With one of those plans, the insurance firm transfers a portion of your month-to-month premium payments right into a money value account. This account earns passion or is invested, helping it expand and give a more significant payment for your beneficiaries.

With a level term life insurance policy policy, this is not the case as there is no cash value component. As a result, your plan won't expand, and your fatality advantage will certainly never increase, thus limiting the payout your recipients will certainly receive. If you desire a policy that gives a death benefit and constructs cash value, consider entire, universal or variable strategies.

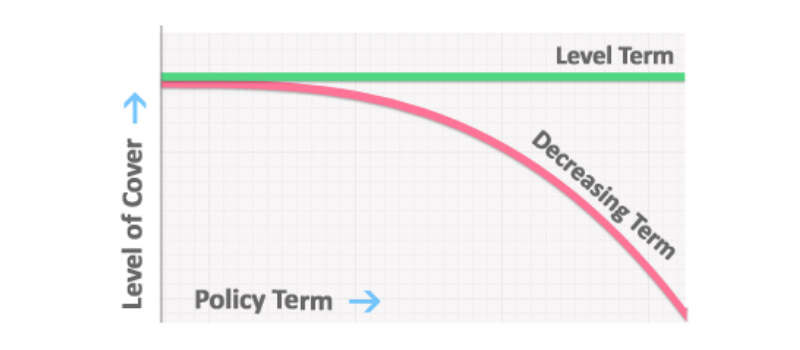

The second your policy runs out, you'll no much longer have life insurance policy protection. Degree term and decreasing life insurance policy offer comparable policies, with the major distinction being the fatality advantage.

It's a type of cover you have for a certain quantity of time, called term life insurance policy. If you were to pass away during the time you're covered for (the term), your liked ones get a set payout agreed when you obtain the plan. You merely pick the term and the cover quantity which you can base, as an example, on the expense of increasing children till they leave home and you might utilize the settlement towards: Assisting to settle your home loan, financial obligations, bank card or loans Aiding to pay for your funeral costs Aiding to pay college fees or wedding celebration expenses for your kids Assisting to pay living expenses, replacing your earnings.

What is Term Life Insurance With Accelerated Death Benefit? An Overview for New Buyers?

The plan has no cash worth so if your settlements quit, so does your cover. The payment continues to be the same throughout the term. For instance, if you get a level term life insurance coverage policy you might: Choose a taken care of quantity of 250,000 over a 25-year term. If throughout this time you die, the payment of 250,000 will be made.

{kind=link}

Latest Posts

Instant Insurance Life Quote Whole

Final Expense Agencies

Funeral Funds For Seniors